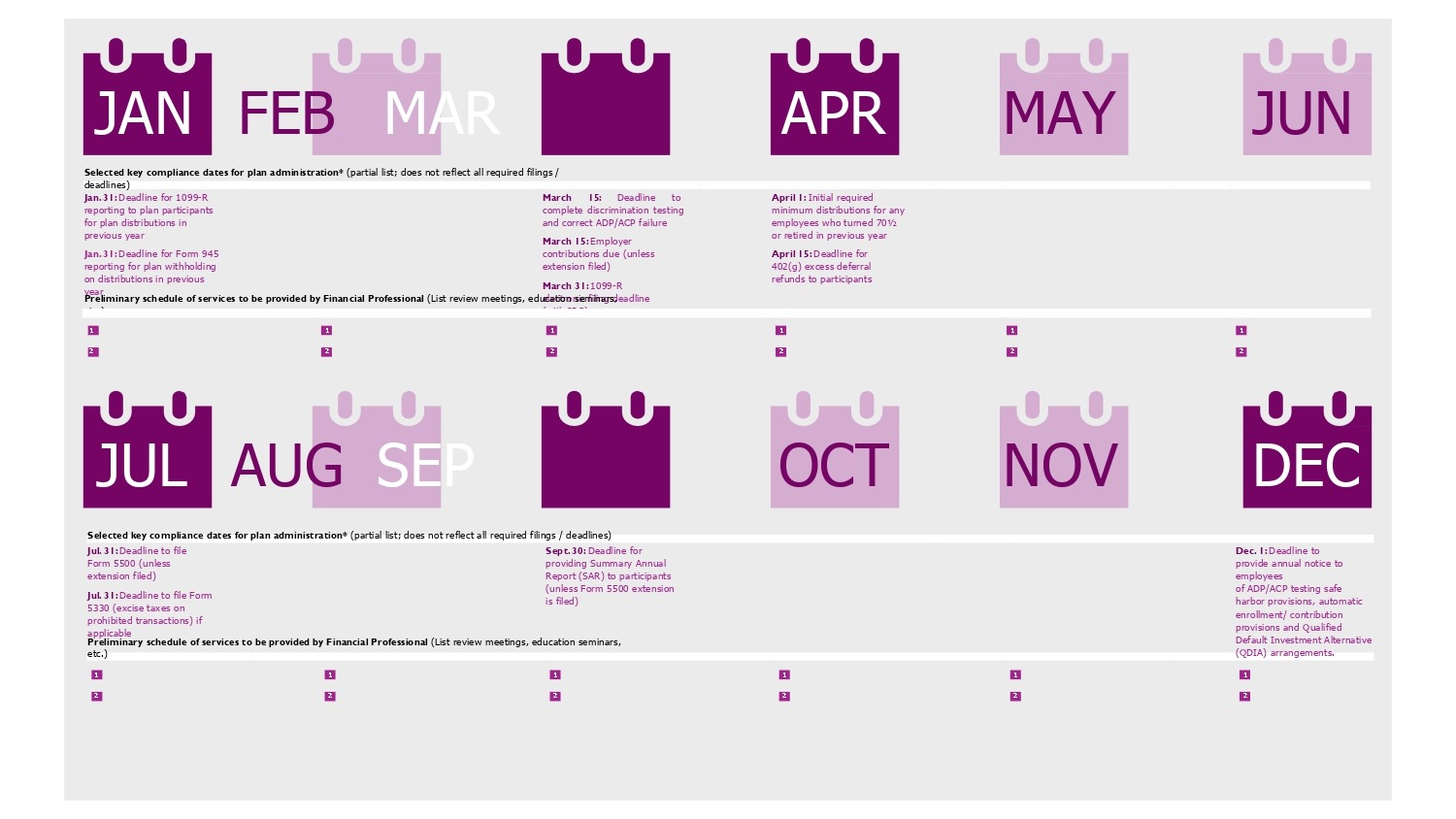

A Fee Policy Statement (FPS) establishes written guidelines that are designed to help plan sponsors and other fiduciaries prudently review the fees and expenses incurred by the plan for services rendered on behalf of the plan.

The fiduciary review of the plan’s services and their related fees under a FPS is intended to supplement the fiduciary review of the plan’s investment vehicles. The plan’s procedures for prudently selecting and monitoring the plan’s investment vehicles may be separately addressed under an Investment Policy Statement (IPS).

A Fee Policy Statement (FPS) establishes written guidelines that are designed to help plan sponsors and other fiduciaries prudently review the fees and expenses incurred by the plan for services rendered on behalf of the plan.

According to the U.S. Department of Labor (DOL), plan sponsors and other responsible fiduciaries must engage in an “objective process” designed to gather certain key information concerning the plan’s service providers and their compensation. As is the

case with an IPS, a plan is not required to maintain an FPS. However, an FPS can serve as an effective tool that can help plan fiduciaries meet these DOL requirements.

Creating an FPS should be done in accordance with the Plan Sponsor’s legal counsel.

An FPS may vary widely from plan to plan, but representative topics that may be covered in a FPS would include:

- The purpose and objective of the plan and FPS Fiduciary duties relating to the plan’s payment of fee

- Roles of the Plan Fiduciary and service providers

- Overview of fiduciary review process

- Gathering information about service providers and their services

- Gathering competitive pricing information

- Comparing provider’s fee against competitive pricing information

- Special considerations for bundled services

- Allocation of plan expenses

- Fee disclosures to participants

FEE POLICY STATEMENT

The purpose of the plan and the FPS

• Identify the plan and the employer sponsoring such plan, as well as the identity of the actual plan fiduciary (the “Plan Fiduciary”) who is responsible for reviewing the plan’s service providers and their fees, which may be the employer itself, a committee or an individual.

• State that the FPS establishes guidelines for prudently reviewing the fees payable by the plan to its service providers.

• Specify that these guidelines also address the required fee disclosures made by providers to responsible plan fiduciaries under Section 408(b)(2) of the Employee Retirement Income Security Act of 1974, as amended (“ERISA”), and the related regulations (the “408(b)(2) Regulations”).

Fiduciary duties relating to the plan’s payment of fees

• Specify that under the plan trust requirements of ERISA, other than paying benefits to participants, plan assets may only be used to pay “reasonable” plan expenses.

• Explain that the Plan Fiduciary must ensure that plan expenses are reasonable, using the skill and care that a prudent person familiar with such matters would use in accordance with the duty of prudence under ERISA.

• State that, in general, the use of plan assets to pay a service provider constitutes a “prohibited transaction” under ERISA, unless the provider delivers fee disclosures to the responsible Plan Fiduciary in accordance with the 408(b)(2) regulations.

• Explain that under DOL rules, the Plan Fiduciary must engage in an “objective process” designed to gather the information necessary to assess: (a) the qualifications of the plan’s service providers; (b) the quality of their services; and (c) the reasonableness of their fees in light of the services provided.

• State that the Plan Fiduciary will review a provider’s 408(b)(2) fee disclosures and all other necessary information using the guidelines in the

FPS.

Roles of Plan Fiduciary and service providers

• Describe the Plan Fiduciary’s role and responsibilities in the selection of the service providers to the plan and approving the use of any plan assets to pay their fees.

• Identify the significant providers of plan services, which may include the following:

⚪ A provider of core recordkeeping services for the plan (the “Recordkeeper”).

⚪ A third-party administrator responsible for compliance testing and other high- level plan administrative services (“TPA”).

⚪ A Financial Professional engaged to assist in the oversight of the plan’s investments (the “Financial Professional”).

• Explain that the Financial Professional, TPA, ERISA counsel or another third-party may assist the Plan Fiduciary in identifying, gathering and interpreting the relevant information in accordance with the FPS.

Overview of fiduciary review process

• Specify that prior to the initial selection of a service provider to the plan, the Plan Fiduciary will:

⚪ Gather all necessary information from the proposed provider.

⚪ Gather competitive pricing information.

⚪ Prudently compare the proposed provider’s compensation against the competitive pricing information.

• Explain that for purposes of monitoring the plan’s existing service providers, the Plan Fiduciary will periodically gather updated information and prudently compare their compensation against competitive pricing information.

• Identify the anticipated frequency of the Plan Fiduciary’s periodic reviews of the existing service providers for monitoring purposes (e.g., once every three years).

Gathering information about service providers and their services

• Specify that the Plan Fiduciary will gather all necessary information concerning the plan’s service providers and their services, which may include the following:

⚪ Qualifications of provider such as a firm résumé, summary biographies of key personnel, the firm’s history and client base.

⚪ Scope and quality of services, such as a written explanation of services, brochures, website information, client referrals and the firm’s policies and procedures.

⚪ Total compensation, including any direct compensation that is invoiced, as well as any indirect compensation that is automatically payable from a plan’s investment vehicles, such as 12b-1 fees or revenue-sharing payments.

Gathering competitive pricing information

• State that the Plan Fiduciary will gather competitive pricing information, which may be obtained as follows:

⚪ Soliciting bids from multiple service providers, including information concerning the provider’s qualifications, as well as the scope and quality of services.

⚪ Benchmarking analysis from a vendor who is able to benchmark the plan’s fees and expenses using market data from an appropriate peer group of plans.

⚪ Survey data from 401(k) trade associations and consulting firms, which typically include survey results from a large number of plans participating in the survey.

⚪ Other sources of informal pricing information, which may be available through financial and benefits professionals, including the plan’s Financial Professional or TPA.

• Explain that the Financial Professional, TPA or another third-party may assist the Plan Fiduciary in gathering and interpreting competitive pricing information in accordance with the FPS.

Comparing provider’s fee against competitive pricing information

• Specify that an evaluation of a service provider’s fee against competitive pricing information involves an “apples to apples” baseline comparison.

• State that the FPS establishes guidelines for prudently reviewing the fees payable by the plan to its service providers.

⚪ A provider’s fee formula may take different forms, including an asset-based fee, a per-participant fee, a per-plan fee or transaction-based fees.

⚪ To draw a baseline comparison of a provider’s fee against the competitive pricing information, all fees should be converted to the

same form (e.g., asset-based fee or per-participant fee).

• State that the reasonableness of a provider’s fees should be evaluated based on all relevant factors, including the quality of the provider’s

services.

⚪ Explain that a provider’s fee should not be deemed to be excessive based solely on a comparison of pricing information only.

⚪ Specify that providers with higher-than-average fees may be utilized, so long as they are appropriate in light of the services provided (e.g., high service quality, responsiveness to inquiries, customized services).

• State that if the Plan Fiduciary concludes that a provider’s fees are excessive in light of the services provided, the Plan Fiduciary may take the following actions.

⚪ Renegotiate the fee.

⚪ Request enhanced or additional services.

⚪ Request any indirect compensation to be credited to a fee recapture account, which may then be utilized for the benefit of the plan and its participants.

⚪ Consider an alternative provider of services.

Special considerations for bundled services

• Explain that certain providers may bundle their offerings of services and/ or investments.

⚪ For example, a mutual fund or insurance platform may be willing to serve as a plan’s Recordkeeper, but only if the plan agrees to use certain investment vehicles offered by such platform.

⚪ As a further example, a Recordkeeper may also offer to serve as the TPA for a plan under a bundled arrangement, eliminating the need to hire a separate “local” TPA.

• Explain that for purposes of evaluating a bundled offering, the Plan Fiduciary may either “unbundle” the relevant offerings and evaluate the fee for each separate offering, or evaluate the integrated fees and expenses for the bundled offering as a whole.

⚪ If evaluating the cost of a bundled offering as a whole, it would be appropriate to compare such cost to those of other bundled offerings for purposes of a baseline comparison.

Allocation of plan expenses

• State that the employer sponsoring the plan will pay all fees and expenses for “settlor” functions relating to the employer’s decision to establish the plan, change the plan design or terminate the plan as required under ERISA.

• Explain that all reasonable fees and expenses related to the operation and administration of the plan may be paid from plan assets, unless and to the extent the plan’s governing document provides otherwise.

• State that if the method for allocating expenses to the accounts of participants is specified in the plan’s governing document, the Plan Fiduciary will ensure the fees of the plan’s service providers are allocated in this manner

⚪ If the allocation method is not specified in the plan’s governing document, the Plan Fiduciary will prudently select a method that has a “rational basis” for how expenses are to be allocated to participants (e.g., asset-based fee, per-participant fee, transaction-based fee) in accordance with DOL guidance.

Fee disclosures to participants

• State that the employer sponsoring the plan will pay all fees and expenses for “settlor” functions relating to the employer’s decision to establish the plan, change the plan design or terminate the plan as required under ERISA